10 minute read

Is Monzo worth it? A review after 9 years as a customer

TL;DR: key takeaways

A first-person Monzo review after nine years as a customer, covering the free account, paid plans, savings rates, travel spending, borrowing, and whether Monzo is actually worth switching to in 2026.

If you just need the link, you can get your Monzo referral code here.

Affiliate disclosure: this post contains a Monzo referral link. If you use it, we both get a mystery reward of £20, £50, or £100. It doesn't change anything about your account.

I opened my Monzo account in May 2017, back when it was still a prepaid card with a coral-coloured debit card and a waiting list. Nine years later, it's my primary bank account. I pay my rent through it, sort my salary into pots on payday, use it abroad without thinking about exchange rates, and have referred enough friends to know that the mystery reward almost always lands at £20.

The question I want to answer here isn't whether Monzo is a good bank; it is. The question is whether it's worth switching to, or whether you're better off staying with whatever you already have. After nine years of daily use, here's what I'd tell someone asking in 2026.

Three things I'd tell you up front

- The free account is genuinely excellent. No monthly fee, instant notifications, pots for budgeting, salary sorting, no foreign transaction fees on card spending, and FSCS protection up to £120,000. Most people don't need to pay for Extra, Perks, or Max.

- The app is still the best in UK banking. I've tried Starling, Chase, Revolut, and Nationwide's app. Monzo's is faster, more intuitive, and more useful for actually managing money day-to-day.

- The paid plans are situational, not essential. Perks (£7/month) is worth it if you hold enough savings for its 0.50% rate boost to cover the fee, or if the partner perks fit your habits. Max (£17/month) is worth it if you travel enough to need the insurance. For everyone else, the free account is the product.

What the free account actually gives you

This is where Monzo earns its reputation. The free current account includes:

- Instant spending notifications: every card payment triggers a push notification within seconds, showing exactly where and how much

- Pots: separate savings buckets within your account for ring-fencing money (bills, holidays, emergency fund)

- Salary Sorter: automatically splits your salary into pots on payday

- No foreign transaction fees on card payments abroad (Mastercard exchange rate)

- Free ATM withdrawals: unlimited in the EEA, £200/month free outside the EEA (then 3%)

- Savings pots at 2.75% AER: instant access, no lock-in

- Bill splitting and Monzo-to-Monzo instant transfers

- Full UK banking licence, FSCS protected up to £120,000

For most people, this is more functionality than their current bank offers, and it costs nothing.

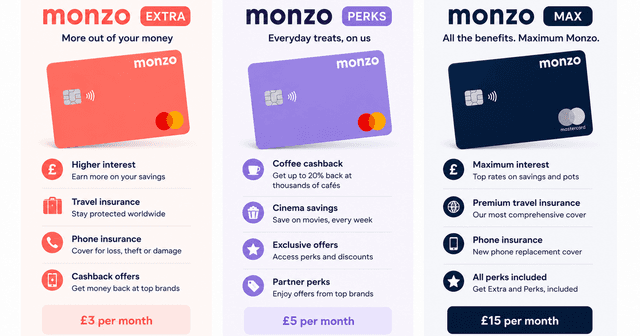

The paid plans: are they worth it?

Monzo's paid tiers are Extra (£3/month), Perks (£7/month) and Max (£17/month). Extra adds tools (virtual cards, connected accounts), Perks adds a 0.50% savings boost plus lifestyle perks, and Max adds the insurance bundle. The break-even maths shifts depending on your savings balance and travel frequency: Perks pays for itself on the rate boost alone at around £16,800 in instant-access savings, while Max no longer has any rate edge over Perks (both pay 3.25% AER), so its case rests entirely on the travel, phone and breakdown cover.

My take: I was on the top-tier plan for a year when I was travelling more frequently. The insurance and travel extras made it worthwhile. When travel slowed down, I dropped back to the free account. Monzo makes it easy to switch: no penalty, no commitment (Max's 3-month minimum aside).

For the full plan-by-plan breakdown with worked maths on each tier, see our Monzo Max review (Max vs Perks vs Extra) →.

Savings rates in context

Monzo's savings rates are competitive but not market-leading:

| Account tier | Instant access rate | How it compares |

|---|---|---|

| Free / Extra | 2.75% AER | Mid-table, above most high-street banks, below best-buy tables |

| Perks (£7/month) | 3.25% AER | The cheapest route to the boosted rate; pays for itself around £16,800 in savings |

| Max (£17/month) | 3.25% AER | Same rate as Perks, but bundled with insurance and lifestyle perks |

The convenience factor matters here. Monzo savings pots are instant access, set up in seconds, and visible alongside your spending. If you'd otherwise leave money in a 0.5% high-street account because you can't be bothered opening a separate savings product, Monzo's 2.75% is a massive upgrade for zero effort.

Spending abroad

This is one of Monzo's strongest features and the reason I always take it travelling.

Card payments: no foreign transaction fees. You get the Mastercard exchange rate, which is consistently close to the mid-market rate. I've used Monzo in Europe, the US, and Southeast Asia. The rate has always been fair.

ATM withdrawals: unlimited and free within the EEA. Outside the EEA, the first £200/month is free, then Monzo charges 3%. For most trips this is fine. If you're withdrawing large amounts of cash in non-EEA countries regularly, Starling or Chase may be better choices.

Compared to traditional banks: most UK banks charge 2.75–3% on foreign transactions. On a two-week holiday with £1,500 in spending, that's £37–£45 in fees you'd avoid with Monzo.

Borrowing: overdrafts and Flex

Overdraft: Monzo offers arranged overdrafts at 39.9% EAR. That's competitive for an app bank (Starling is similar) but expensive in absolute terms. Monzo does one thing well here: it shows your overdraft cost in real-time in the app, so you always know exactly what you're paying. No surprises.

Monzo Flex: a buy-now-pay-later feature built into the app. Split purchases into 3 monthly instalments at 0% interest, or longer plans at 18–30% APR. The 3-month option is genuinely useful for spreading larger purchases without cost. I've covered Monzo Flex in detail separately. The short version is that the 3-month plan is good, the longer plans are expensive.

The app experience

I've used Monzo daily for nine years. The app is fast, well-designed, and consistently updated. Key things that work well in practice:

- Search: you can search all transactions by merchant, amount, or category. Useful for finding that one payment from three months ago.

- Spending categories: automatic categorisation that's right about 90% of the time, with the ability to correct it

- Trends: month-by-month spending breakdowns that actually help you spot patterns

- Connected accounts: you can link other bank accounts (Starling, Chase, traditional banks) to see all your money in one place

What doesn't work as well: customer support wait times vary. In-app chat is usually fast (under 10 minutes in my experience), but I've had waits of 30+ minutes during busy periods. Phone support exists but isn't Monzo's strength.

Who Monzo is best for

Best for:

- People who want to actually manage their money, not just store it

- Frequent travellers (no foreign transaction fees)

- Anyone currently paying fees or getting poor rates at a high-street bank

- Freelancers and small business owners (see our Monzo Business review)

- Couples who want a Monzo joint account with good budgeting tools

Less ideal for:

- People who need branch access regularly

- Anyone who prefers phone support over app-based chat

- Heavy cash users outside the EEA (ATM limits apply)

If you fit one of those but otherwise like Monzo, the cleanest move isn't to switch. Keep Monzo as your primary and open a second account for the gap: Chase for cashback, Starling for cheaper overdrafts and non-EEA ATMs, Nationwide for branches, Revolut for multi-currency. The best second UK bank account to pair with Monzo post walks through the maths for each.

The referral bonus

Monzo's refer-a-friend scheme gives both you and the referrer a Monzo mystery reward of £20, £50, or £100. You need to sign up using a referral link and make any card payment within 30 days. The reward lands in your account within a few days.

In my experience referring friends, the reward has been £20 every time. The £50 and £100 tiers exist but are rare. Still, £20 of free money for opening a free bank account is hard to argue with, and it's the biggest potential payout of any UK bank's referral scheme: we've compared all of them in our best UK bank referral bonuses roundup.

Get your Monzo referral code here →

Monzo FAQs

Is Monzo worth it in 2026?

Yes, for most people. The free account gives you instant spending notifications, budgeting pots, salary sorting, no foreign transaction fees, and FSCS protection up to £120,000, all with no monthly fee. Nine years in, it's still my primary bank account. The paid plans (Extra at £3/month, Perks at £7/month, Max at £17/month) are harder to justify unless you specifically need the higher savings rate or travel insurance.

Is Monzo safe to use as a main bank account?

Yes. Monzo holds a full UK banking licence, is FCA-regulated, and your deposits are protected by the FSCS up to £120,000. It has over 10 million UK customers and has been operating since 2015. The lack of physical branches is the only structural difference from a traditional bank.

Is Monzo better than a traditional bank?

For everyday banking, yes. The app is faster, spending notifications are instant, pots make budgeting easier, and there are no foreign transaction fees. Where traditional banks still win: branch access, cheque deposits (Monzo now supports this via the app, but it's slower), and some mortgage providers prefer to see salary going into a traditional bank account.

Is Monzo Extra, Perks, or Max worth paying for?

Monzo Extra (£3/month) is worth it for virtual cards and connected accounts; it no longer carries a savings-rate edge over the free plan. Perks (£7/month) adds a 0.50% savings boost (3.25% AER instant access) plus lifestyle rewards, and the boost alone covers the fee at around £16,800 in savings. Monzo Max (£17/month) adds worldwide travel insurance, phone insurance, breakdown cover and discounted lounge entry: worth it if you travel frequently and would otherwise buy those separately.

What are the downsides of Monzo?

No physical branches. Free ATM withdrawals outside the EEA are capped at £200/month (then 3% fee). The overdraft rate is 39.9% EAR, competitive for an app bank but expensive in absolute terms. And if you rely on phone support, wait times can be longer than in-app chat.

The bottom line

Monzo is worth it. The free account alone (instant notifications, pots, salary sorting, no foreign fees, 2.75% savings, FSCS protection) is better than what most UK banks offer on their paid products. After nine years, it's still my primary account, and I've never seriously considered switching away.

The paid plans are worth it in specific circumstances (enough savings for Extra, enough travel for Max) but the free account is the core product, and it's genuinely good.

If you're still on a traditional bank account with no budgeting tools, slow notifications, and foreign transaction fees, switching to Monzo is one of the easiest financial upgrades you can make. It takes about 10 minutes, and you don't need to close your old account.

Referral Plug founder · Personal finance writer and UK consumer savings specialist

I specialise in finding people the best deals to cope with the ever-increasing cost of living. I like to review companies from everyday industries like banking and energy and try to provide a fresh mix of facts and unbiased opinions.

Last verified: June 2026 · Last updated