10 minute read

Best second UK bank account to pair with Monzo (2026)

TL;DR: key takeaways

Which account to open alongside Monzo, by use case. Chase UK for cashback, Revolut for travel and investing, Starling for cheaper overdrafts and travel ATMs, Nationwide for branches. Plus the single account I'd add if I could only pick one.

If you just need the link, you can get your Monzo referral code here.

Affiliate disclosure: this post contains a Monzo referral link. If you use it, we both get a mystery reward of £20, £50, or £100. It doesn't change anything about your account.

I've been a Monzo customer since May 2017, and the question I get asked more than any other is some version of "which second account should I open alongside it?" The premise is right. Monzo is a strong primary current account, but it isn't the best at everything, and there's nothing stopping you from running a second account in parallel.

The honest answer depends on what you'd actually use the second account for. There are four sensible scenarios, with a different best pick for each. This post lays them out with the maths, then ends with the single account I'd open if I could only add one.

Quick comparison

| If your second account is for... | Pick | Why |

|---|---|---|

| Earning cashback | Chase UK | 2% on groceries, transport, fuel & eating out; capped at £20/month |

| Travel and investing | Revolut | 30+ currencies, fractional shares, full UK licence since March 2026 |

| Cheaper overdrafts, travel ATMs, a fixed-rate saver | Starling | 15-35% EAR vs Monzo's 39.9%, £300/day non-EEA ATMs, 3.70% AER 1-year fix |

| Branch access | Nationwide FlexDirect | 600+ branches, 5% AER on the first £1,500 for year one |

If you only ever add one second account, I'd pick Chase UK. Reasoning below.

Why bother with a second account at all?

You don't have to. Monzo handles 95% of normal banking on its own: salary, bills, pots, spending, free travel abroad, FSCS protection up to £120,000. For most people, Monzo is enough.

A second account starts to make sense when one of these is true:

- You spend £500+/month on groceries and fuel and aren't earning cashback on any of it (a few hundred pounds a year of free money on the table).

- You hold £5,000+ in savings and want a better return than Monzo's 2.75% AER on the free plan (a fixed-rate product, or an intro-boosted rate).

- You spend abroad in non-GBP currencies regularly, or have foreign-currency income. Monzo only operates in GBP.

- You want to invest in stocks or crypto from inside your banking app. Monzo doesn't really do this yet.

- You sometimes need to walk into a branch. Monzo has no branches at all.

If none of those apply, save yourself the admin and stop here.

Option 1: Chase UK (best for cashback)

The cleanest secondary-account pick. Chase pays 2% cashback on groceries, transport, fuel, restaurants, cafes and takeaways, capped at £20/month. The cap kicks in once your qualifying spending hits £1,000/month. For someone spending £800/month on those categories, that's roughly £192/year of free money, as long as you make 15+ payments and keep £1,000 in a Chase saver each month.

Chase also pays 4.5% AER for 12 months on its boosted Saver (a 2.25% intro bonus on top of the 2.25% variable base), and 5% AER on the round-up account ongoing. On a £5,000 savings balance, Chase's year one earns about £88 more than Monzo's 2.75%.

How to pair it with Monzo: salary into Monzo, set up a standing order topping Chase up by £100-200 a week for groceries, fuel and eating out. Spend on the Chase card for those categories, everything else on Monzo, and keep £1,000 in a Chase saver so you stay eligible. The cashback lands monthly. After 12 months, reassess the savings rate. Monzo's ongoing 2.75% beats Chase's drop-to 2.25%.

Catches: Chase has no overdraft, no joint account, no Monzo-style budgeting. To earn cashback you must make 15+ payments a month and keep £1,000 in a Chase saver, and there's no cashback on overseas spending. Not a primary, but an almost-free upgrade if you can be bothered to switch which card you tap at Tesco.

For the head-to-head, see Monzo vs Chase UK.

Option 2: Revolut (best for travel and investing)

Revolut became a properly licensed UK bank in March 2026, which closes the old FSCS gap. What it adds to a Monzo setup is breadth, not depth: 30+ currencies you can hold in-app, fractional stock trading, crypto, and a 2% non-EEA ATM fee (vs Monzo's 3%) above the free monthly allowance.

The trade-off on free Revolut is the £1,000/month FX limit. Once you exceed it, Revolut charges 1% on any further currency exchange. For most UK holidaymakers spending under £1,000/trip on the card, this is a non-issue. For frequent travellers, digital nomads, or anyone who genuinely needs to hold euros or dollars, Revolut earns its place. For everyone else, Monzo's no-limit Mastercard rate is simpler.

How to pair it with Monzo: Monzo as primary (salary, bills, budgeting), Revolut as the pre-trip and investing card. Before a trip, transfer over and convert to the destination currency at the interbank rate. After the trip, transfer leftover GBP back. Use Revolut for any stocks or crypto exposure you want inside a banking app.

Catches: Revolut's free-tier savings rate is mediocre. Investment fees on Standard are notably worse than dedicated brokers (Trading 212, Freetrade), and crypto fees are 1.49% unless you upgrade. If your second-account use case is purely cashback or savings, Revolut isn't the right pick.

For the head-to-head, see Monzo vs Revolut.

Option 3: Starling (best for cheaper overdrafts, travel ATMs, and fixed-rate savings)

Starling is the most Monzo-like product on this list. Same full UK banking licence, same FSCS £120,000 protection, same fee-free travel card spending, same in-app chat support. But its savings pitch has weakened: Starling scrapped current-account interest in early 2025, and its instant-access Easy Saver pays 2.50% AER, below Monzo's free 2.75%. Where Starling still beats Monzo on the free tier is:

- 15-35% EAR on overdrafts (vs Monzo's flat 39.9%): the clearest, most consistent win.

- £300/day free non-EEA ATM withdrawals, no monthly cap (vs Monzo's £200 per 30 days, then 3%): the second clearest win, and the reason I opened Starling alongside Monzo in January 2026 ahead of an upcoming trip.

- 3.70% AER on the 1-year Fixed Saver (Monzo has no fixed-rate option), with a £2,000 minimum and the money locked in for the full term.

- Virtual cards without a paid plan (Monzo puts them behind the £3/month Extra plan).

On a £10,000 savings balance, Starling's 1-year fix earns about £95 more than Monzo's instant-access rate, in exchange for locking the money away for the year. On instant access, Monzo now pays more than Starling, so don't open Starling expecting a better savings rate on cash you might need to touch.

How to pair it with Monzo: salary into Monzo, spend on Monzo (the budgeting tools are still best-in-class), and use Starling for any overdraft buffer, cash withdrawals abroad, or money you can lock into the Fixed Saver for the term. Keep flexible savings in Monzo pots, where the rate is actually higher.

Catches: running two app-only banks both designed to be your primary is genuinely confusing. There's a real risk of "which app has the bill in it" friction. If you don't run an overdraft, don't withdraw cash abroad, and don't have £2,000+ to lock in, the gains may not justify the friction.

For the head-to-head, see Monzo vs Starling. Starling has also just started trialling a refer-a-friend scheme that pays new customers £25 in a Space after their first card payment; it's new enough that we haven't been able to test it yet, and our Starling referral page tracks its status.

Option 4: Nationwide FlexDirect (best for branch access)

Nationwide is the secondary account if you want anything physical. 600+ branches, real staff, paper statements if you want them. As a building society it also runs the Fairer Share scheme, which has paid eligible members up to £100/year when profits allow.

The current account itself, FlexDirect, pays 5% AER on the first £1,500 for the first 12 months, plus 1% cashback on debit card purchases (£5/month cap) for the same first year. To qualify you need to pay in £1,000/month. After year one, the rate drops to 1% AER and the cashback ends.

How to pair it with Monzo: redirect £1,000 of your salary into Nationwide monthly to qualify for the interest and cashback. Use Nationwide for branch banking, paying cheques in, the rare cash deposit, and as a backup if a digital bank ever has an outage. Use Monzo for everything else.

Catches: the 5% headline is on a £1,500 cap, so the absolute interest earned is about £75/year. Nationwide's app is decent but generations behind Monzo's. The Visa debit carries standard foreign transaction fees so you'd never use it abroad. The reason to pick Nationwide is structurally that branches exist, not that the rate is amazing.

For the head-to-head, see Monzo vs Nationwide.

If you can only add one, add Chase

The cashback maths is real money you can feel within the first month, the year-one savings bonus is the biggest of any free account I've seen, and there's almost nothing to manage. Salary stays in Monzo, you just tap Chase at the supermarket and the fuel pump.

- Revolut wins if you have an active reason to hold foreign currencies. Otherwise Monzo's free FX is enough.

- Starling wins on overdraft pricing, travel ATM withdrawals and fixed-rate savings, but those only matter if you'd actually use them; its instant-access rate now trails Monzo's, and the cognitive overhead of two near-identical banks is real.

- Nationwide wins on branches, which most people under 40 won't use.

Chase wins the most generic case: a UK household that spends on groceries, transport and fuel and would rather get 2% back than not.

How to actually run a Monzo + second account setup

Three things to get right:

- Don't split your salary across both. Send the whole salary to Monzo (or whatever your primary is), then push fixed amounts to the second account by standing order. This keeps your main budget in one place and avoids the "where's my money this month" problem.

- Set a clear job for each card. Chase for groceries and fuel. Revolut for trip spending. Starling for overdraft buffer and cash withdrawals abroad. Nationwide for branch days. Don't try to remember edge cases in the moment.

- Reassess every 12 months. Chase's cashback now requires 15+ payments a month and £1,000 kept in a Chase saver, and the savings bonus expires after year one. Nationwide's intro rate drops after year one. Renew the setup or pull out.

Best second bank account FAQs

Can I have a Monzo account and another bank account at the same time?

Yes. There's no UK rule against holding multiple current accounts. Many people run two or three. There's no fee for opening another as long as your credit footprint isn't already heavily concentrated in new accounts.

Does opening a second account hurt my credit score?

A new current account adds a hard credit search and a new line on your file. One additional account is unlikely to move your score meaningfully if you're otherwise stable. Opening three or four current accounts in a short period can.

Will opening a second account close my Monzo?

No. Opening a new bank account doesn't close any existing one. The Current Account Switch Service (CASS) does close your old account when you switch, but you don't need to use CASS to open Chase, Revolut, Starling or Nationwide alongside Monzo. Open them as additional accounts and Monzo stays exactly as it is.

Is there a downside to having two current accounts?

Two: the admin (two apps, two cards, two sets of statements) and the dilution of any deposit-linked perks that require a monthly minimum (Chase cashback after year one, Nationwide interest). If you keep one as the clear primary and tightly scope the second, the downside is small.

Which second account is best for someone who travels a lot?

If you mostly travel within Europe, Monzo on its own is usually enough (free EEA ATMs, no FX limit). If you regularly travel outside the EEA or work in foreign currencies, Revolut is the strongest second pick because of the multi-currency wallet and lower ATM overage fee (2% vs Monzo's 3%).

Which second account is best for savings?

It depends on the type of savings. For flexible, instant-access cash, Monzo's free-tier 2.75% AER actually beats Starling's Easy Saver at 2.50% AER (an old "Starling for higher savings" idea no longer holds for flexible cash). For a fixed-term lock-in of £2,000+, Starling's 1-year Fixed Saver at 3.70% AER outperforms anything Monzo offers. Chase is the strongest short-term play (4.5% AER on the boosted Saver for the first 12 months only). Beyond a year, dedicated savings platforms (Trading 212 Cash ISA, easy-access savers from Atom or Zopa) typically beat all four.

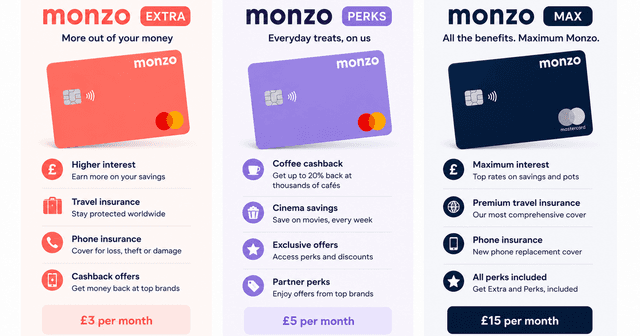

Should I just upgrade to Monzo Max instead of opening a second account?

Possibly. Monzo Max (£17/month) bundles worldwide travel insurance, phone insurance, breakdown cover, discounted airport lounge entry via LoungeKey, and a 3.25% AER savings rate. If you'd otherwise pay for those separately, Max can be cheaper than buying them piecewise. It doesn't earn cashback on groceries, though, so a Monzo + Chase setup is still the better fit when cashback is the goal. (See our Monzo Max review for the maths.)

The bottom line

A second bank account isn't compulsory. But the right one earns you money for tapping a different card at the till. If you only add one, make it Chase. If you have a specific use case (travel, savings, branches), pick the one that fits.

Sign-up rewards are thin on the ground among these four picks. Chase, Revolut and Nationwide run no refer-a-friend scheme at all, and Starling has only just started trialling a £25 one, which we haven't been able to test yet. The UK banking brands with tested schemes are ranked in our best UK bank referral bonuses guide.

Whatever you pair Monzo with, keep Monzo as the primary. After nine years it's still the cleanest day-to-day banking app in the UK, and the budgeting tools are what stop the second-account setup from getting messy.

You might also like

- Is Monzo worth it? An honest review after 9 years

- Best UK bank account for travelling abroad

- Best UK bank account for freelancers

If you're opening a Monzo account, using a Monzo referral code gets you a mystery reward of £20, £50 or £100 when you make your first card payment within 30 days.

Referral Plug founder · Personal finance writer and UK consumer savings specialist

I specialise in finding people the best deals to cope with the ever-increasing cost of living. I like to review companies from everyday industries like banking and energy and try to provide a fresh mix of facts and unbiased opinions.

Last verified: June 2026 · Last updated