6 minute read

Why MoneySavingExpert recommends Chase over Monzo for cashback

TL;DR: key takeaways

MoneySavingExpert treats Chase as the answer for cashback and Monzo as the answer for budgeting. Here's exactly what MSE says about both, the maths behind their position, and where this guide agrees and disagrees with them.

If you just need the link, you can get your Monzo referral code here.

Affiliate disclosure: this post contains a Monzo referral link. If you use it, we both get a mystery reward of £20, £50 or £100. It doesn't change anything about your account.

If you read MoneySavingExpert's digital banking guide (opens in new tab) looking for a clear "Monzo or Chase" verdict, you won't find one. What you'll find is a split: Chase is positioned as the cashback pick, Monzo as the budgeting pick, and MSE explicitly suggests holding both. This post walks through what MSE actually says, the maths behind their position on Chase cashback, and where my own Monzo vs Chase comparison agrees and disagrees.

What MSE actually says about each bank

MSE's best digital bank accounts (opens in new tab) guide groups Monzo, Chase and Starling together as the leading challengers. Their summary positions:

- Chase: "Best for cashback." 2% on groceries, transport, fuel, and now restaurants, cafes and takeaways. Capped at £20/month. Plus 4.5% AER for 12 months on the boosted Chase Saver and 5% AER on the separate round-up account.

- Monzo: "Best for budgeting." Pots, salary sorting, spending targets and real-time notifications. MSE highlights Monzo's user-polling results: 80% rated it "great" for usability and 85% rated it "great" for features, the highest feature rating in their digital bank comparison.

- Starling: "Best for overseas ATM use." No withdrawal limits abroad (Monzo's free account caps at £200/month outside the EEA).

Martin Lewis himself doesn't single out one as the outright winner. His on-record framing is closer to "the best account is the one that fits how you actually bank." MSE's structural advice across these guides is consistent: the answer to "which digital bank?" is usually "one of them as your main account and one of them alongside it for the perks you'd otherwise miss."

Why MSE points at Chase specifically for cashback

The reason Chase is the cashback pick rather than Monzo is simple: Monzo's free account doesn't pay cashback at all. Monzo's paid tiers offer Billsback, but that's a lottery (random monthly payout on a household bill, with most months returning small amounts) rather than guaranteed cashback. For predictable earnings on everyday spending, the only meaningful comparison among the digital banks MSE covers is Chase.

Chase's cashback structure (opens in new tab), as MSE flags it:

- 2% cashback on groceries (most supermarkets), transport (TfL, rail tickets, taxis, fuel), restaurants, cafes, takeaways and EV charging points

- Capped at £20/month (i.e. 2% cashback on the first £1,000 of qualifying spending in those categories), with no cashback on overseas spending

- Ongoing, not a 12-month intro (the old 1% new-customer deal was withdrawn in mid-2026)

- You qualify each calendar month by making 15+ card payments or Direct Debits and keeping £1,000+ across your Chase savers

MSE's framing on this is balanced. They flag both the upside (guaranteed money on spending you'd do anyway, capped but real) and the caveats: most households won't hit the £20/month maximum because most households don't spend £1,000/month specifically on those categories, and the monthly criteria add friction.

The cashback maths MSE encourages you to run

MSE consistently steers readers toward running the actual numbers on cashback offers rather than reacting to the headline. Their general principle: only count guaranteed cashback after subtracting any fees or required behaviour change, and ignore optimistic best-case caps.

For Chase specifically:

| Monthly spend in qualifying categories | Annual cashback |

|---|---|

| £300 (low) | ~£72 |

| £600 (average UK household groceries plus fuel) | ~£144 |

| £800 (groceries, fuel and the odd takeaway) | ~£192 |

| £1,000 (the cap) | £240 (the maximum) |

The cap matters. The 2% headline rate sounds like an unlimited boost on your spending; in practice it's capped at £240/year, and you only hit that ceiling if a) you spend at least £1,000/month in the qualifying categories specifically, b) you remember to use the Chase card rather than your phone wallet pointed at a different card, and c) you clear the monthly criteria (15+ payments and £1,000 kept in a Chase saver). For most UK households the realistic cashback is £150 to £240 per year, with the upper end being homes with two cars, regular rail commuting, eating out and a major weekly shop on the Chase card.

That number is real, but it's not transformational. MSE's framing reflects that: Chase is a sensible secondary card for cashback, not a reason to upend a primary banking relationship.

Where my position differs from MSE's framing

MSE's coverage is even-handed and built for a wide audience. My Monzo vs Chase comparison takes the same data and lands in a more opinionated place: Monzo as primary, Chase as the cashback card alongside it. The reasons:

- Chase doesn't offer overdrafts, joint accounts, or any credit product. A bank that declines payments when you tap empty isn't suitable as a primary current account for most people. MSE acknowledges this in their feature tables but doesn't lean on it as hard as I would.

- Monzo's budgeting tools are genuinely structural. Salary Sort, pots, spending targets and Bills Pots aren't garnish; they change how money behaves in your account. Once you're using them, switching primary banks means giving them up. MSE's coverage flags this but treats it as a preference rather than a structural advantage.

- The cashback maximum is small relative to either bank's switching incentives. Chase's £240/year ceiling is meaningful, but the year-one savings boost (4.5% AER on the Chase Saver for 12 months) is often the bigger number on a five-figure savings balance. MSE flags both; I'd weight the savings rate more heavily.

The split-the-difference setup MSE implies (and which I recommend explicitly) is the same in both places: salary and Direct Debits into Monzo, top up Chase weekly, tap Chase at the supermarket, the petrol pump and when you eat out, leave everything else on Monzo. You capture the cashback (~£192/year for typical household spending, provided you make 15+ payments and keep £1,000 in a Chase saver each month), the year-one savings bonus, and Monzo's pots and salary sorting.

What MSE caveats about both Chase and Monzo

MSE's broader caveats on digital banks apply to both:

- Customer service is app-and-chat only. No phone line, no branches. Both banks struggle on complex cases more than on routine ones.

- Savings rates aren't best-in-class long-term. Chase's headline 4.5% is a 12-month bonus; after that it drops to 2.25%. Monzo's free 2.75% is reasonable but below the best-buy instant-access tables. MSE consistently flags that "top-pick savings usually pay more" in standalone accounts.

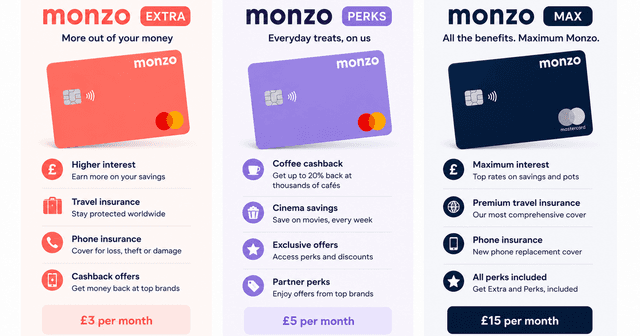

- Packaged plans need careful maths. Monzo's Extra (£3/month), Perks (£7/month) and Max (£17/month) only pay off if you'd use the included features. MSE's general advice on paid banking plans applies cleanly.

Should you trust MSE's view here?

MoneySavingExpert is the UK's largest consumer-finance site and operates independently of the banks it reviews. Their methodology (user polling for satisfaction, structured feature comparison, and Martin Lewis's editorial line on "best account is the one that fits how you bank") is the most rigorous publicly available framework for choosing a digital bank.

If MSE rates Chase highly on cashback and Monzo highly on budgeting, both signals are credible because the same methodology applied across all providers would surface different winners if the underlying products were weaker.

What MSE won't tell you is whether Monzo's referral bonus is worth claiming. That part's straightforward: if you're going to open a Monzo account anyway, using a referral link adds a mystery reward of £20, £50 or £100 at zero cost. Chase doesn't run a public referral programme, so there's no equivalent on that side.

MSE on Chase vs Monzo FAQs

Does MoneySavingExpert recommend Chase or Monzo?

MSE doesn't pick an outright winner. Their digital banking guide treats both as leading challenger banks with different strengths: Chase for cashback and the year-one savings bonus, Monzo for budgeting tools and salary sorting. Martin Lewis's framing is "the best account is the one that fits how you actually bank," and MSE's structural recommendation is usually to hold both alongside each other rather than choose one.

How much cashback can you actually earn on Chase?

Chase pays 2% cashback on groceries, transport, fuel, restaurants, cafes, takeaways and EV charging, capped at £20/month, as long as you make 15+ payments and keep £1,000 in a Chase saver each month. The realistic annual cashback for a typical UK household is £150 to £240, depending on how much of your spending falls into the qualifying categories. You only hit the £240/year maximum if you spend £1,000/month specifically on those categories and consistently use the Chase card rather than a phone wallet pointed at a different card.

Why doesn't Monzo offer cashback on the free account?

Monzo's free account is built around budgeting tools (pots, salary sorting, spending targets) rather than transactional perks. Cashback would require Monzo to either accept lower interchange margins or build a more complex earnings structure into the free tier. Monzo's paid tiers offer Billsback, which is a lottery-style payout on household bills rather than guaranteed cashback. For predictable cashback, Chase is the better fit.

Does MSE think you should switch your salary to Chase?

No. MSE's coverage flags Chase's structural gaps (no overdraft, no joint account, no Flex-equivalent borrowing product) and doesn't position it as a primary account for most people. The usual MSE framing is to keep your salary going into a more fully-featured account (Monzo, Starling or a traditional bank) and top up Chase weekly for the qualifying spending categories.

Is Chase or Monzo better for travel?

Both are excellent for travel. Both use the Mastercard exchange rate with no foreign transaction fees on card spending. Chase has the edge on ATM withdrawals abroad (£1,500/month fee-free vs Monzo's £200/month outside the EEA, then 3%). For card-only travellers, the two are functionally identical abroad. For more detail, see the best UK bank account for travelling abroad.

Should you trust MSE's view on Chase and Monzo?

Yes, with the usual caveat that MSE's coverage is built for a wide audience and your specific situation (overdraft needs, joint account, travel patterns, how much you'd actually spend in cashback categories) decides the answer. MSE is the most independent and rigorously-sourced UK consumer finance publisher in this space; their digital banking ratings are credible signals, not personal advice.

You might also like

- Monzo vs Chase: cashback or better budgeting?

- Is Monzo worth it? An honest review after 9 years

- Best second UK bank account to pair with Monzo

Sources

- MSE best digital bank accounts:

https://www.moneysavingexpert.com/banking/digital-banking/(opens in new tab) - Chase UK cashback terms:

https://www.chase.co.uk/gb/en/banking/cashback/(opens in new tab) - Monzo plans page:

https://monzo.com/i/plans/(opens in new tab) - FCA Financial Services Register:

https://register.fca.org.uk/s/(opens in new tab)

Referral Plug founder · Personal finance writer and UK consumer savings specialist

I specialise in finding people the best deals to cope with the ever-increasing cost of living. I like to review companies from everyday industries like banking and energy and try to provide a fresh mix of facts and unbiased opinions.

Last verified: June 2026 · Last updated